The Numbers Behind the Strategy Shift

The world’s 100 largest mining companies generated $946.4 billion in sales during 2024, with a collective market value reaching $1.83 trillion by mid-2025. But size alone doesn’t guarantee success in today’s environment.Between January and July 2025, the sector witnessed over $47 billion in major transactions—each valued above $1 billion. These weren’t opportunistic plays. They were calculated moves to build scale, capture strategic assets, and position for long-term resilience:

- Anglo American’s acquisition of Teck reshaped the diversified mining landscape

- Gold-focused consolidations including Gold Fields/Osisko Mining (C$2.2B) and Coeur Mining/SilverCrest Metals (C$2.3B) reinforced the flight to quality

- Africa’s emergence as a strategic jurisdiction, highlighted by AngloGold Ashanti’s C$2.5B Centamin acquisition under the continent’s Green Minerals Strategy

- China’s downstream expansion through Zijin Mining’s US$1B purchase of Newmont’s Akyem mine

The pattern is clear: companies are spending, but only where it counts.

The Realities CEOs Can’t Mine Around

Yet beneath the deal-making, fundamental challenges persist—and they’re getting harder to ignore:

Capital scarcity has become the norm, except for top-tier gold projects. Permitting timelines stretch years, not months. Rising costs and declining ore grades compress margins even as metal demand accelerates. And perhaps most critically, trust—between miners, investors, governments, and communities—has become the sector’s scarcest resource.

Many companies are now revisiting dormant projects, reassessing what’s genuinely shovel-ready versus what was optimistically labeled as such. But increasingly, the constraint isn’t about finding ore bodies. It’s about processing capacity.

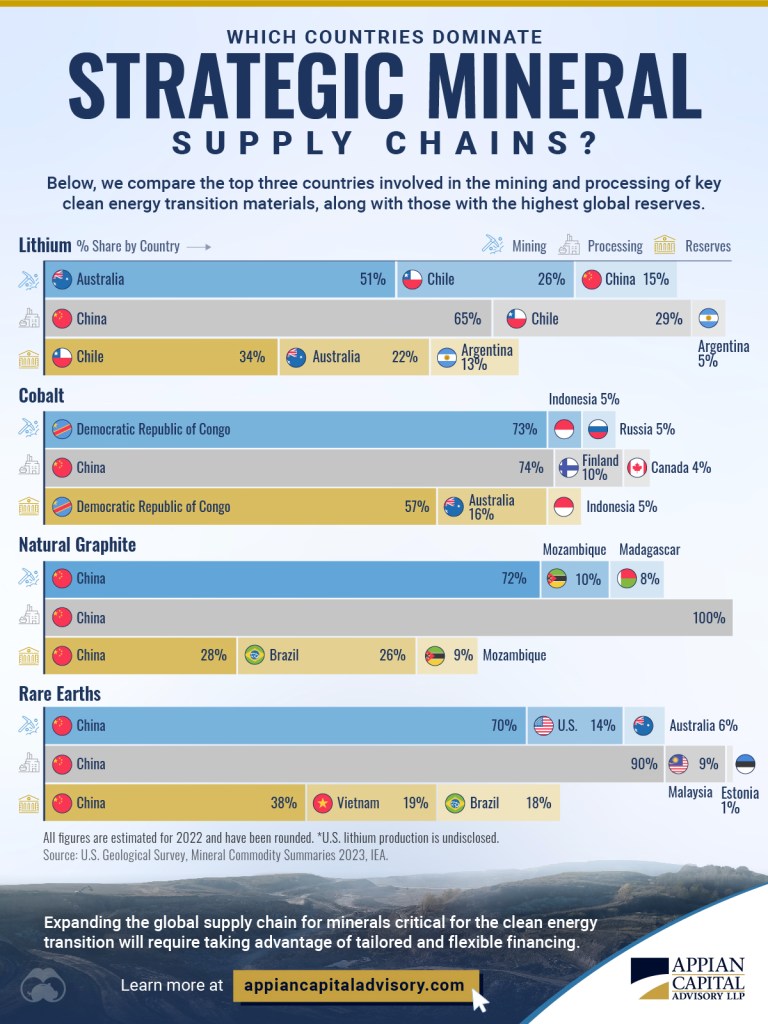

The Refining Bottleneck No One Can Ignore

China controls the vast majority of global mineral processing infrastructure. Recent reports suggestion that China controls more than 90% of the global output of refined rare earths and that continues to impose national security and economic risk for the rest of the world. This isn’t a competitive disadvantage—it’s a geopolitical vulnerability. As Western nations scramble to establish domestic refining capacity (the U.S. administration has proposed an 18-month timeline for a new facility for political purposes), the mining industry’s midstream dependency has become a matter of national security, not just supply chain efficiency.

Canada’s Moment—and Mining’s Imperative

Amid this turbulence, one bright spot stands out: Canada has reclaimed mining’s legitimacy as a pillar of national economic strategy. Critical minerals and energy transition metals aren’t niche topics anymore—they’re central to Canada’s industrial policy and global competitiveness.

This shift illustrates something essential: mining companies that succeed in the next decade won’t just be good operators. They’ll be sophisticated navigators of the external landscape.

The Public Affairs Imperative

The lesson for mining executives is stark: technical excellence and financial discipline are table stakes. What differentiates winners from losers is the ability to read—and respond to—the world beyond the mine gate.

- Geopolitical shifts that redefine supply chains overnight

- Regulatory frameworks that enable or strangle projects

- Community relationships that determine social license

- Policy trends that create or close windows of opportunity

- Media narratives that shape investor confidence and public trust

Mining has always operated at the intersection of geology and economics. But today, it operates at the intersection of geology, economics, and geopolitics. CEOs who treat public affairs as an afterthought—or worse, as a compliance function—will find themselves outmaneuvered by competitors who understand that stakeholder engagement, government relations, and strategic communications are core competencies, not support functions.

The mining companies thriving today aren’t just the ones with the best deposits or the strongest balance sheets. They’re the ones who understand that external realities shape internal possibilities. They’re the ones investing in relationships as deliberately as they invest in infrastructure. They’re the ones who see public affairs not as cost centres or risk mitigation, but as competitive advantage.

In an industry where trust is currency and uncertainty is the operating environment, mining leaders must become as fluent in the language of public affairs as they are in reserve calculations and processing recovery rates.

The ore bodies haven’t changed. The world around them has. And that demands a different kind of leadership.

Leave a comment